A new framework for stress-testing investment portfolios against nature-related shocks

Can nature risk be measured as financial risk? Joel Johannes-Gold, Nicola Ranger and Anne Marie Eikeset present a new framework designed to estimate the financial impact of nature-related shocks on individual companies, and the results from a pilot study.

Research by Earth Capital Nexus and partners has suggested that nature-related shocks could trigger macroeconomic losses comparable to, or exceeding, those of the 2008 financial crisis. Companies and investors exposed to sectors such as agriculture, food and beverages, utilities, construction and mining face the most direct vulnerability, but the risk extends well beyond these sectors through supply chains and trade linkages.

There is no widely adopted method for measuring nature-related financial risk at the company level in a way that is consistent across sectors and geographies. This means that currently, investment portfolios cannot be stress-tested for nature shocks, and investors are unlikely to factor nature risk into their valuation of companies. Broader market failure may result, with capital markets exacerbating the wider economic costs of natural capital loss.

The new collaboration between Earth Capital Nexus and Norges Bank Investment Management (NBIM), the asset manager of the Norwegian sovereign wealth fund, aims to assess how companies’ dependencies on natural capital could affect their financial performance. Building on the Nature Value at Risk (NVaR) framework co-developed by the Earth Capital Nexus team and the European Central Bank, and using NBIM’s publicly available global equity holdings, we are applying NVaR at the company level, estimating how individual companies may be impacted by plausible nature stress scenarios.

A missing link: from macro risk to portfolio exposure

Most work on nature-related financial risk has focused on the national or sectoral level. Less attention has been given to how these risks transmit to individual companies and, by extension, to the shareholders of those companies.

This matters for investors like NBIM, which manages a global portfolio of more than 7,000 stocks. Without company-level analysis of nature-related financial risk, it is difficult for investors to see where material exposure may sit within their portfolios. NBIM recently released its Nature expectations of companies. As a financial investor, it wishes to support companies to focus on reporting more quantitative, business-relevant information to understand how nature-related factors affect their activities and cash flows. As part of this, NBIM is also engaging with academic partners – including Earth Capital Nexus – and data vendors to help develop frameworks and tools for understanding how nature-related factors affect corporate activities and cash flows across all sectors and geographies in a consistent way.

While existing nature scores available to investors typically rate company policies or supply chain exposure qualitatively, NVaR expresses risk in terms of potential revenue loss under a defined stress scenario, based on each company’s activities, geographical footprint and supply chain. Under a 1-in-25-year water scarcity scenario, for example, a food manufacturer in a water-stressed region could lose 26% of its revenues.

As a first step, we have applied the NVaR framework to a subset of 10 companies, using NBIM’s global equity holdings as a proxy portfolio for assessing how institutional investors holding globally diversified equities may be affected by nature-related financial risk.

Mapping nature risk through the value chain

To derive company-level NVaR results, we have developed an approach for assessing how nature risk transmits through a company’s value chain, based on its structure, activities and specific vulnerabilities. We trace risk from upstream suppliers (Scope 3) through direct operations (Scope 1) to end markets, considering shocks across five ecosystem services that are highly material across a wide range of economic sectors: groundwater, surface water, water quality, air quality and pollination. To ground these results, we first map out where we expect nature risks to emerge, as illustrated for two large companies in very different sectors: agri-foods and technology.

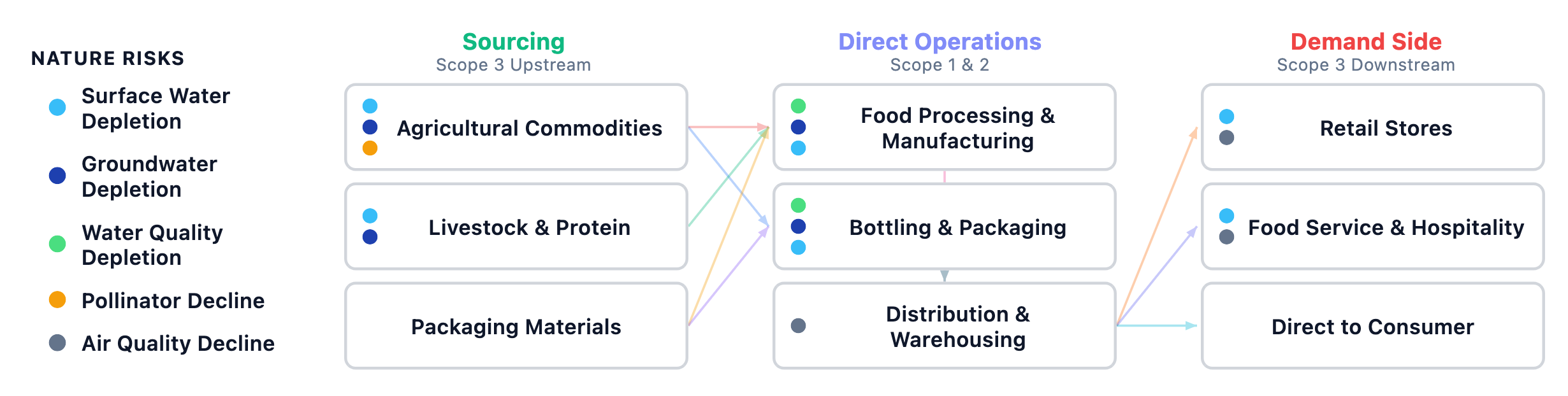

Agrifood Company A – nature risk scoping

Mapping this company’s direct operations reveals a high dependence on bottling and food processing factories for its revenues. In turn, these assets are heavily reliant on both ground and surface water as an ingredient, and for cleaning and cooling.

Figure 1. Value chain mapping for Agrifood Company A

Tracing the upstream supply chain reveals a network of agricultural commodity producers across multiple crop and livestock categories. A stable water supply is crucial to maintain yields for these commodities, many of which are grown in water-stressed regions. Certain crops are also highly dependent on pollinators, with research showing that coffee yields could drop by 10–40% without them. The company and its supply chains are also influenced by wider market factors that may themselves be affected by nature risks, including labour productivity, operating costs (including energy and cooling costs), regulatory costs and the changing cost of capital.

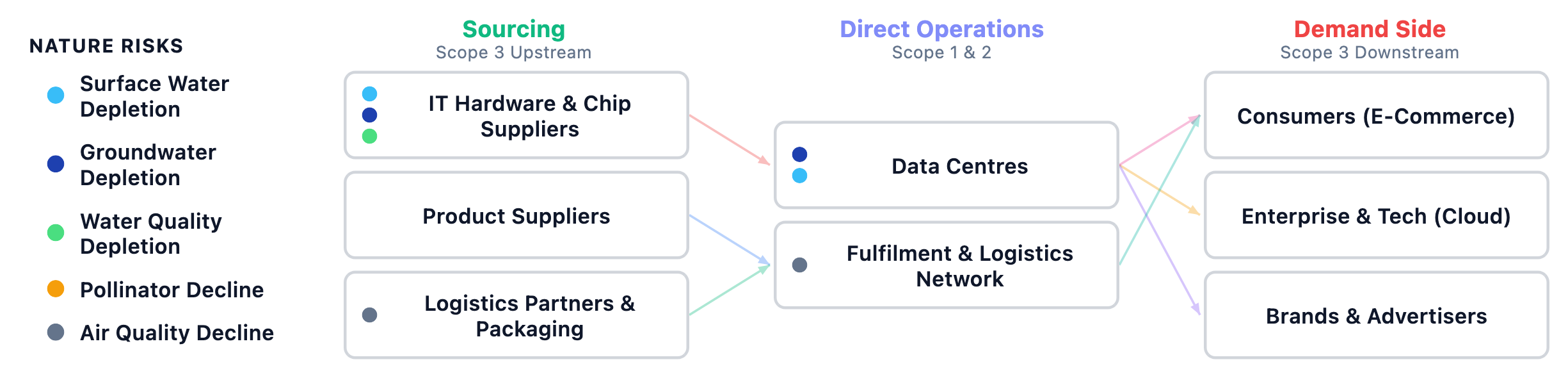

Tech Company A – nature risk scoping

While many technology companies have historically faced limited physical risks from their own operations, a growing number are expanding into data centres, a sector highly dependent on ground and surface water for cooling. Many data centres are also dependent on sourcing energy from utilities, a sector with high water dependency. For Company A, the fastest-growing part of its operations is data centres, which underpin its internet hosting services business.

Figure 2. Value chain mapping for Tech Company A

Nature risk also sits in the supply chain. Semiconductor manufacturing, a key input for data centre hardware, is one of the most water-intensive industrial processes. The supply base for advanced chips is highly concentrated, with manufacturing facilities located in water-stressed regions. A severe groundwater shortage affecting this concentrated manufacturing base would likely carry significant financial risk downstream.

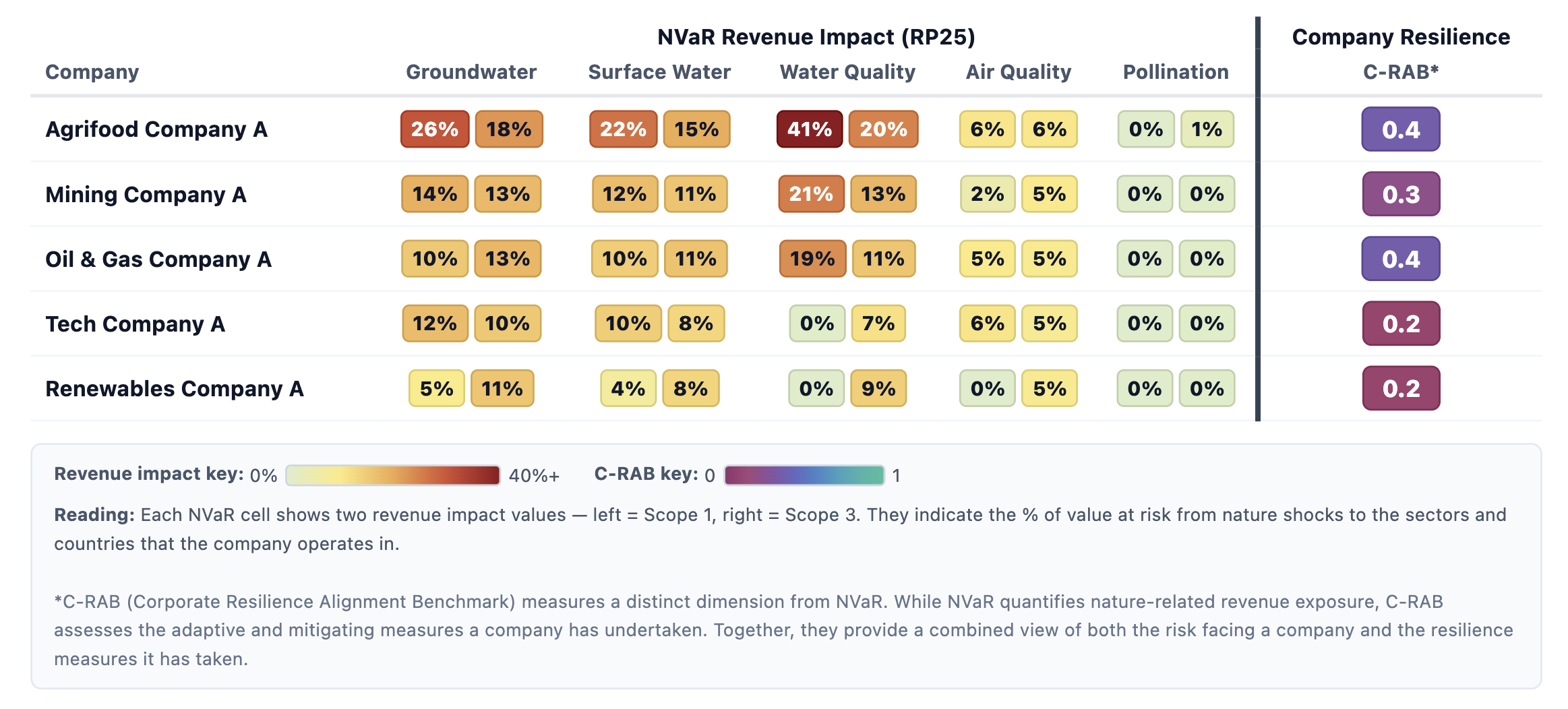

How big are the risks? A comparison across sectors

Applying the NVaR approach to our company-level framework and drawing on data from Bloomberg and FactSet, we have completed a preliminary assessment of risks for a subset of companies in NBIM’s global equity holdings. The five companies shown below were selected to capture a range of sectors, geographical footprints and company sizes.

Figure 3. Assessment of company-level nature value risk for five companies

The analysis suggests that Agrifood Company A faces the greatest nature-related risk across all five ecosystem services examined. Under a 1-in-25-year (RP25) groundwater stress scenario, Scope 1 revenue losses could reach 26%, reflecting the highwater dependency of food processing and bottling activities in the regions where the company operates. We also find water quality to be a notable Scope 1 risk for the mining and oil and gas companies, reflecting the strict water purity requirements of ore processing and refinery cooling systems.

Tech Company A and Renewables Company A score comparatively low on Scope 1 risk, though Renewables Company A faces greater exposure through its upstream supply chain, where the manufacturing of solar panels and wind turbines is more water-intensive than power generation itself.

The value of granular asset-level data

The primary determinants of nature risk at the company level are the sector a company operates in and its specific vulnerabilities. But geography matters too. Agrifood Company A has operations spread across water-stressed regions including Brazil, India, Sub-Saharan Africa and parts of Asia-Pacific, together accounting for over a third of its total asset base. Mining Company A is also operating in comparatively high-risk regions, with the majority of its assets located in Southern and Sub-Saharan Africa and Latin America. By contrast, the assets of Tech Company A and Renewables Company A are overwhelmingly concentrated in the United States, which, while not free of water stress, faces lower average exposure.

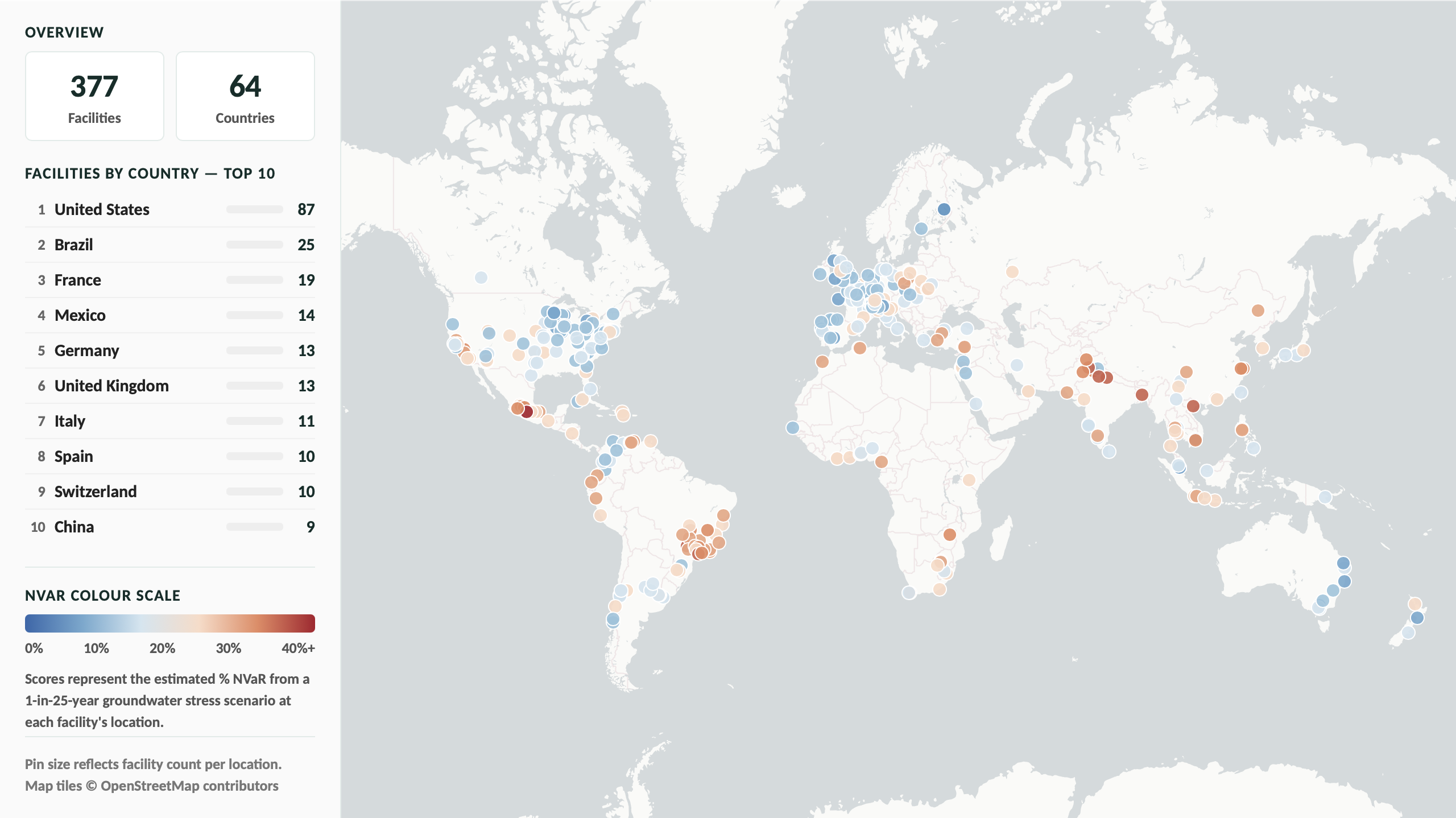

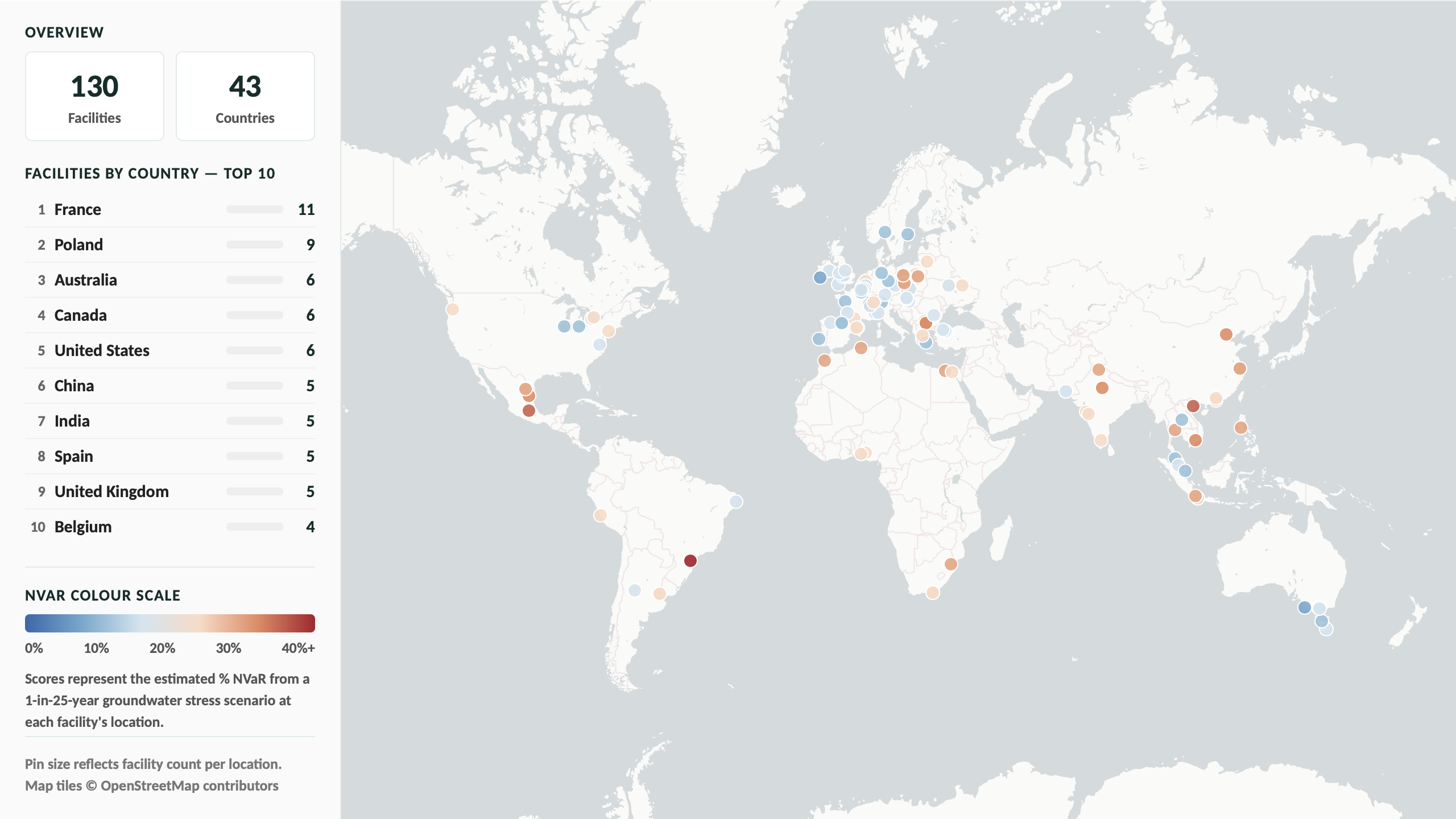

But nature risk can vary as much within a country as between countries, making facility-level location data important. To test this, we mapped the manufacturing and food processing facilities of two agrifood companies against our granular NVaR geospatial data – see Figures 4 and 5.

Figure 4. Facility-level groundwater NVaR for Agrifood Company A

Figure 5. Facility-level groundwater NVaR map for Agrifood Company B

Our mapping reveals significant variation at the facility level. Individual plants in central Mexico, northern India and parts of Southeast Asia face groundwater potential revenue risks of above 40%, while facilities in Northern Europe and parts of Oceania sit below 15%. This variation is invisible at the country-average level, underscoring the importance of granular asset location data in producing accurate estimates of nature risk at the company level.

Company preparedness matters

NVaR gives an objective measure of the risks faced by a company given its sector, asset and revenue structures and spatial characteristics, but it does not provide information on how well prepared that company is. This is where a complementary tool developed by the EarthCap team, Corporate Resilience Alignment Benchmark (C-RAB), plays an important role. C-RAB assesses company disclosures to evaluate where a company sits relative to its peers in terms of its management of nature-related dependencies and its preparedness. Together, NVaR and C-RAB provide a holistic view of company-level nature risk.

What this enables for investors and where next

This pilot provides a new dimension for stress testing: quantifying how much revenue is at risk at the company level from nature shocks. It highlights the importance of understanding how nature risk transmits through individual companies, of incorporating asset-level data, and of using granular ecosystem-based risk metrics rather than aggregate indicators. It demonstrates that it is possible, based on current data and open methods, to construct globally consistent risk assessments of relevance to institutional investors, surfacing risks that are important for inclusion in long-term valuation models.

This type of analysis can also facilitate engagement between investors and companies on nature-related risks and opportunities. Portfolio managers can engage on specific, financially grounded terms, benchmarking a company’s nature-related exposure against sector peers and pressing for a credible plan to address any gap. As regulators and central banks increasingly require nature-related risk disclosure, companies that have not built resilience will face growing scrutiny and, potentially, valuation compression.

Earth Capital Nexus aims to provide analysis and results of companies across NBIM’s global equity holdings by mid-2026, having successfully tested this approach on 10 companies across different sectors and markets. To scale up this work, Earth Capital Nexus is actively looking to partner with data providers who can enhance the coverage, granularity and accuracy of the underlying inputs. Please contact j.z.johannes-gold@lse.ac.uk for more information. A full-length academic paper expanding on these findings will be available in summer 2026.

Joel Johannes-Gold is a Research Assistant and Nicola Ranger Executive Director of Earth Capital Nexus. Anne Marie Eikeset is a former Lead Researcher at NBIM.